Form 3-NDFL is a tax return that must be submitted to the Federal Tax Service by all citizens who independently received income in 2018 (sold property, received large gifts, rented out housing). Please note: a new form must be used for 2019. How to fill out the 3-NDFL declaration for 2018 and how this report for ordinary individuals differs from the declaration submitted by individual entrepreneurs, lawyers and notaries - answers in the material on the site.

Personal income tax must be paid to the state by all citizens receiving income in Russia. Typically, tax agent organizations are involved in withholding tax and transferring it to the budget. These are the taxpayers' employers or those organizations that paid them income. These same tax agents report to the Federal Tax Service on the amounts paid and the tax withheld from them. However, if a citizen has received income independently and does not have a tax agent for any transaction, and also if he is an individual entrepreneur on the general taxation system, he is obliged to report and pay the tax himself. From the article you will learn how to fill out 3-NDFL, when to submit it, and you will be able to download a sample form.

What is Form 3-NDFL

Declaration 3-NDFL was approved by Order of the Federal Tax Service of Russia dated October 3, 2018 No. ММВ-7-11/. The changes are related to large-scale amendments made to Chapter 23 of the Tax Code of the Russian Federation regarding deductions and taxation of real estate of individuals. Taxpayers must report for 2018 on a new form, so it is important to familiarize yourself with the features of filling it out.

The current declaration has decreased in volume compared to the form used before 2019: it is now a form consisting of 13 pages, including a traditional title page and two main sections. In this case, the first section takes only one page, and all respondents must fill it out, and the second section, together with applications (the number of which is 8), takes 9 pages, but they are filled out only if there is information that should be indicated in them, in depending on the taxpayer status.

The personal income tax return is an annual reporting form, but it is intended not only to inform the Federal Tax Service about income received for the purpose of paying tax on them, but also for possible receipt of tax deductions.

Who should submit this report?

Filling out the 3-NDFL declaration is mandatory when receiving income on which it is necessary to calculate and pay personal income tax, as well as to receive a refund of part of the tax previously paid to the budget. According to the requirements of the Tax Code of the Russian Federation, the personal income tax declaration at the end of the year must be submitted by:

- individual entrepreneurs (IP) on the general taxation system;

- lawyers and notaries who have established private offices;

- heads of farms (peasants);

- tax residents of the Russian Federation who received income in other countries in the reporting year (these are persons who actually resided in Russia for at least 183 days a year, but received funds from foreign sources outside its borders);

- citizens who received income from leasing their property or from executing GPC agreements (provided that the customer did not fulfill the duty of a tax agent). In addition, a tax return for personal income tax (form 3-NDFL) is submitted upon sale of property. Although it is mandatory to declare the receipt of income in this case, tax will have to be paid provided that the taxpayer owned it for less than the established minimum period of three years. As for real estate, you will need to pay income tax when selling an apartment (house):

- owned for less than 5 years, if acquired after 01/01/2016;

- owned for less than 3 years, if the property was purchased before 01/01/2016 or received by inheritance, as a gift, under a lifelong maintenance agreement with a dependent, as a result of privatization.

Citizens who win the lottery or sports betting must also pay tax on the amount of their winnings, however, in relation to them, the tax agents are the organizers of these promotions and sweepstakes, who paid them the amount of the winnings. However, if the gift was received in kind, the winner must pay tax on it themselves. In this case, he will also need to fill out and submit a report.

Deadline and methods for submitting the report

The general deadline for submitting the report is April 30 of the year following the reporting year. There are three ways to send a report to the tax service at the taxpayer’s place of registration:

- submit a report directly to the Federal Tax Service inspection in person or through a representative;

- send a paper form by mail;

- Submit your report online on the tax service website or using special services.

The deadline applies only to individual entrepreneurs, lawyers, heads of peasant farms, notaries and citizens declaring income. In order to receive a tax deduction, the declaration can be submitted at any convenient time.

Features of the declaration

When filling out the report form, you must not make mistakes or corrections; in addition, you can only use black or blue ink if the form is filled out by hand. In this case, you need to pay special attention to the different requirements for manual and machine filling out the form:

- When filling out the form by hand, all text and numerical fields (full name, tax identification number, amounts, etc.) should be written from left to right, starting from the leftmost cell, in capital printed characters according to the model that can be found on the Federal Tax Service website . The letters should be even and as similar to the sample as possible. If after filling out the line there are empty cells left, dashes should be placed in them to the very end of the field. If any field is left blank, all its cells must also have dashes.

- Filling out the 3-NDFL declaration on a computer requires aligning all numerical values to the right. It is recommended to use only the Courier New font with a size set between 16 and 18.

If one page of a section or form sheet is not enough to fully reflect all the information, you need to use the required number of additional pages from the same section.

Both in handwritten and printed versions of the report, all amounts must be indicated in kopecks. The exception is the amount of the tax itself, which must be rounded to full rubles according to the usual arithmetic rule - if the amount is less than 50 kopecks, then they are discarded, starting from 50 kopecks and above, they are rounded to the full ruble. Income or expenses that are calculated in foreign currency according to documents must be converted into rubles for inclusion in the report at the exchange rate of the Central Bank of the Russian Federation on the date of their actual receipt. The information provided in the declaration must be confirmed by documents, copies of which are attached to the declaration. To list the documents attached to the 3-NDFL, you can create a register in any order.

All pages of the form must be numbered in order by filling out the “Page” field, starting with 001 (title page). The number of pages must be indicated on the title page, as well as the number of additional documents.

Other applications give:

- codes of income from sources in the Russian Federation and located outside the country;

- object name codes (for example, apartment or land plot);

- codes of the type of taxpayer claiming a tax deduction;

- transaction type codes.

Sample of filling out 3-NDFL for individual entrepreneurs

Title page

In the “TIN” section on the title page and all other pages, you must indicate the correct identification number of the taxpayer - the respondent. If the report is submitted for the first time, then in the column “Correction number” you should indicate 000, and if a document that has already been corrected is submitted again, then the serial number of the correction should be entered in this column. In the “Tax period (code)” column, you need to indicate the code of the reporting period; for annual reporting, this is code 34. If the declaration is not submitted for a year, then you need to indicate the following values:

- first quarter - 21;

- half-year - 31;

- nine months - 33.

The “Reporting tax period” field is intended to indicate the year for which income is declared. In addition, you need to correctly fill out the column “Submitted to the tax authority (code)”, in which you need to enter the four-digit number of the tax authority with which the taxpayer is registered. In this code, the first two digits are the region number, and the last are the direct Federal Tax Service inspection code.

An important field that you need to pay attention to when preparing the title page is the taxpayer category code in the 3-NDFL declaration. All values used are given in Appendix No. 1 to the procedure for filling out the report. Here are some of them:

- IP - 720;

- notary - 730;

- lawyer - 740;

- individuals without individual entrepreneur status - 760;

- farmer - 770.

About himself, the taxpayer must provide his last name, first name, patronymic, date of birth (full), place of birth (as written in the passport), and data from the passport itself. You no longer need to provide your permanent address of residence.

Identity documents have their own coding system, which is given in Appendix No. 2 to the procedure for filling out the reporting form:

- passport of a citizen of the Russian Federation - 21;

- birth certificate - 03;

- military ID - 07;

- temporary certificate issued instead of a military ID - 08;

- passport of a foreign citizen - 10;

- certificate of consideration of an application for recognition of a person as a refugee on the territory of the Russian Federation on the merits - 11;

- residence permit in the Russian Federation - 12;

- refugee certificate - 13;

- temporary identity card of a citizen of the Russian Federation - 14;

- temporary residence permit in the Russian Federation - 15;

- certificate of temporary asylum in the Russian Federation - 18;

- birth certificate issued by an authorized body of a foreign state - 23;

- ID card of a Russian military personnel, military ID of a reserve officer - 24;

- other documents - 91.

The “Taxpayer Status” field is intended to indicate residence; the number 1 in it means that the taxpayer is a resident of the Russian Federation, and the number 2 means a non-resident of the Russian Federation. Also on the title page you need to indicate the total number of sheets in the report, sign and date it was completed.

If the report is submitted through a representative, then his full data must be indicated. In addition, such a person must attach to the 3-NDFL declaration a copy of a document confirming his authority.

Filling out the remaining sheets of 3-NDFL

Of the remaining sheets, the taxpayer must fill out those that contain information. It is only mandatory for everyone to fill out Section 1 “Information on the amounts of tax subject to payment (addition) to the budget/refund from the budget.” It must contain the relevant data on the amount of personal income tax or deduction.

When filling out this section, you need to pay attention to indicating the correct BCC for tax payment and its type. It did not change in 2019. In addition, please note that you must indicate your last name and initials on each completed page, as well as its serial number.

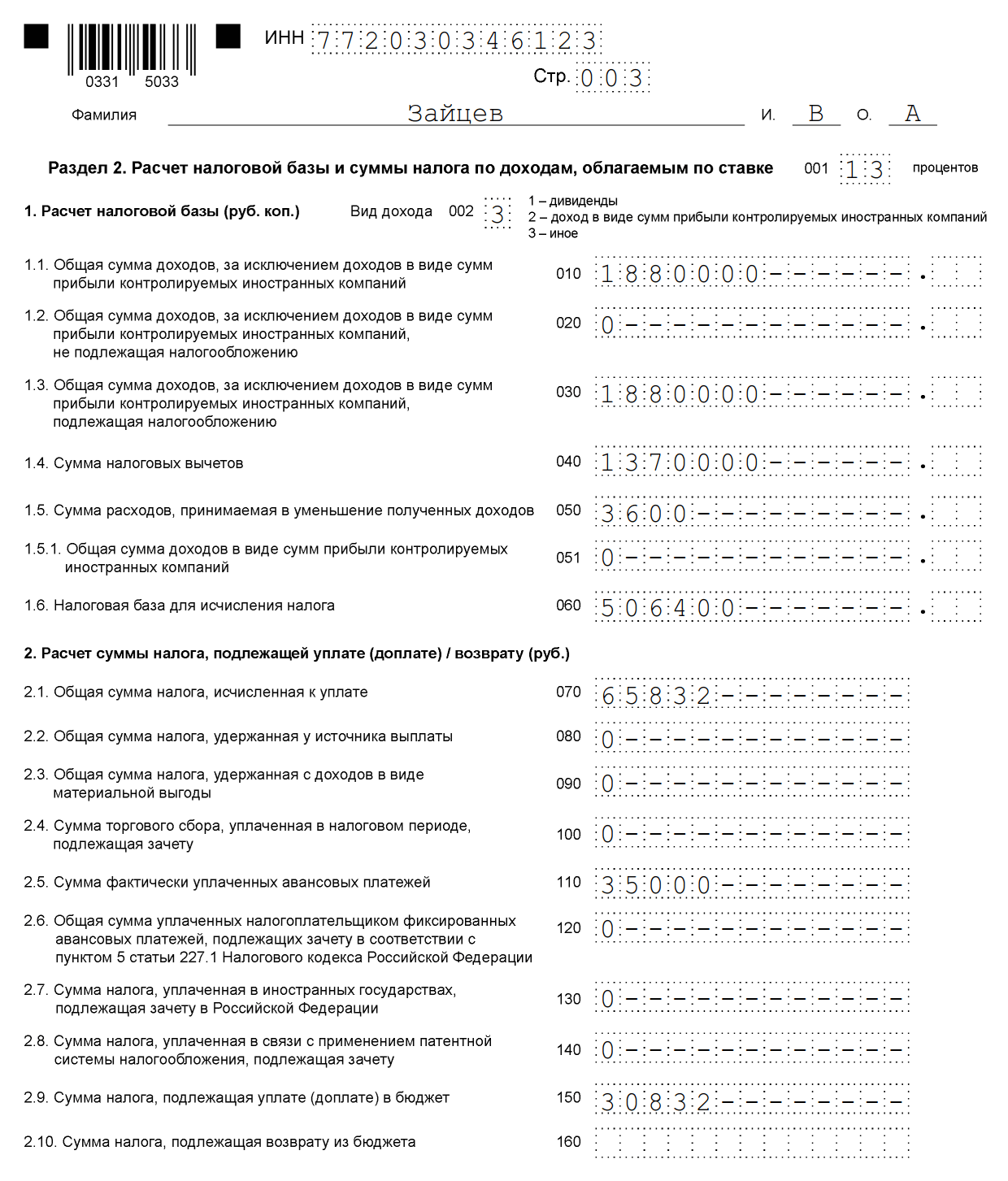

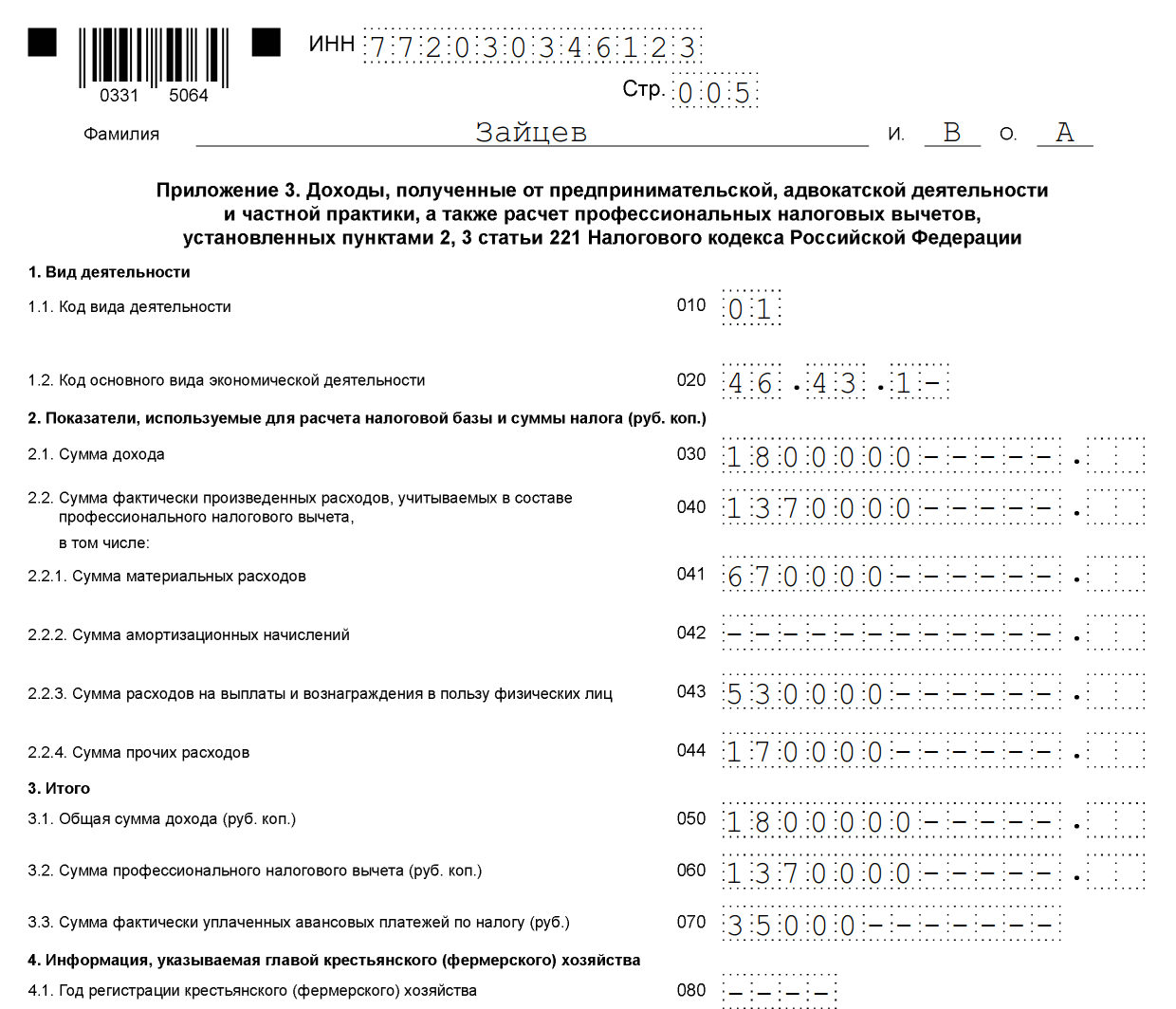

As an example of filling out 3-NDFL, you can give the data of an individual entrepreneur on the general taxation system. In 2018, this individual entrepreneur received income from business activities in the amount of 1,800,000 rubles. In addition, he has the right to apply a professional tax deduction in the amount of 1,370,000 rubles. It included:

- material costs - 670,000 rubles;

- payments under employment contracts - 530,000 rubles;

- other expenses - 170,000 rubles.

For 2018, the individual entrepreneur transferred 35,000 rubles to the budget. advance payments for personal income tax. An entrepreneur is a participant in an investment partnership based on an agreement. And he received income from the sale of securities that were in his ownership for less than three years.

The individual entrepreneur must fill out the title page of the declaration and section 1. In addition, he fills out section. 2, Appendices 1, 3 and 8.

Section 2

Appendix 1 “Income from sources in the Russian Federation”

Appendix 3 “Income received from business, advocacy and private practice”

Appendix 8

Sample of filling out declaration 3-NDFL 2019 for individuals

Let's look at how to correctly fill out the 3-NDFL declaration for an individual who is not registered as an individual entrepreneur. Regardless of what income a citizen declares and whether he intends to ask for a tax deduction, he will have to fill out the title page, sections 1 and 2 of the form. Information is recorded in the declaration attachments if necessary.

Fill out the applications:

- 1 and 7 - when applying for a tax deduction when purchasing real estate or a deduction in connection with the payment of a mortgage;

- 1 and 6, as well as the calculation to Appendix 1 - when declaring income from the sale of real estate and other property;

- 1 - when renting out real estate;

- 1 and 5 - when applying for a tax deduction for treatment, education;

- 1 and 5, as well as the calculation to Appendix 5 - to obtain a deduction for costs under insurance contracts (life, pensions).

As an example, let’s look at a situation where citizen Vitaly Andreevich Volkov sold a house for 2.4 million rubles, which he owned for less than 5 years (bought after 01/01/2016). He must pay tax at a rate of 13%, but in order to reduce the tax base, he immediately issues a tax deduction in the amount of 1 million rubles. He enters the data in the title page, sections 1 and 2, appendices 1 and 6, as well as in the calculation for appendix 1.

It is recommended to fill out the declaration specifically from the calculation and appendices 1 and 6, and then fill out the title page and sections, and indicate page numbers. This is especially important if you write down all the data manually, because you cannot correct anything in the finished declaration.

We fill out the calculation for Appendix 1 (line by line):

- enter the TIN, surname and initials;

- Leave the page number for now;

- 010 - column for indicating the cadastral number of the property. Contained in property documents, you can find out for free in the Rosreestr database;

- 020 - enter the cadastral value of the property as of January 1 of the year in which the property was purchased. If the property has not been assessed as of the specified date, a dash is added;

- 030 - income received from the sale based on the contract;

- 040 - if data on the cadastral value is available, it is multiplied by a factor of 0.7. If field 020 is empty, then 040 is left empty;

- 050 - line to indicate the taxable amount. Select the larger value from fields 030 and 040.

Let's move on to Appendix 6, which indicates all the tax deductions that the taxpayer is counting on. If a citizen has documents confirming expenses for the sold property, then he fills out field 020. If they do not, line 010. If the taxpayer does not claim other deductions, then the value indicated in columns 020 or 010 is transferred to field 160.

Appendix 1 begins with the TIN, surname and initials of the taxpayer. Next we enter:

- 010 - tax rate. For residents - 13%, for non-residents - 30%;

- 020 - codes for the type of income are listed in Appendix No. 3 to the procedure for filling out the declaration. In the case of declaring income received from the sale of real estate, code “01” or “02” may be used. “01” is indicated if the amount of income under the contract (field 030 of the calculation to Appendix 1) is greater than the cadastral value multiplied by a factor of 0.7 (the value entered in field 040). Code “02” is written if the value in column 040 is greater than in column 030;

- fields 030-060 are intended to indicate information about the buyer. If there are no detailed data, it is enough to enter the last name, first name, and patronymic of the new owner;

- in column 070 you need to transfer the value that was recorded in line 050 of the calculation to Appendix 1;

- field 080 is left blank because the buyer is not a tax agent and cannot withhold tax.

Section 2 specifies the income from which the tax will be taken, the tax base and the amount of personal income tax. To do this write:

- 001 - 13 or 30 percent, depending on the residence of the taxpayer (see field 010 of Appendix 1);

- 002 - type of income - 3;

- in columns 010 and 030 - the value of field 070 of Appendix 1;

- the value of field 160 of Appendix 6 is rewritten in line 040;

- the value 060 is calculated as the difference between the values 030 and 040. If a negative number is obtained, set to 0.

- the values of fields 070 and 150 are also calculated. To do this, the figure from the line is 060 × 13%;

- all other columns remain empty.

What remains is Section 1 and the title page. They are filled out according to the algorithm described in the example declaration for individual entrepreneurs.

Section 1

Title page

After all the pages are completed, they must be counted and entered on the title page, as well as numbered. In our example, we ended up with a 6-page declaration. Additionally, you need to clarify the number of sheets of attached documents or their copies. All that remains is to sign all completed declaration sheets (not just the title sheet) and put the current date.

Each taxpayer must independently choose what he needs to fill out and send the completed report to the Federal Tax Service.

Online filling

It is not difficult to fill out 3-NDFL online; to do this, you must have a registered personal account as an individual taxpayer. The login and password for this service can be obtained from the Federal Tax Service after specifying all personal data during registration.

Many operators of accounting services offer users convenient programs for filling out a report online for its subsequent sending over the Internet or printing in paper form. This method is preferable for those taxpayers who are far from accounting and have no experience in filling out reports. However, no special knowledge is required to correctly enter data into this form.

Penalties for non-payment of tax and errors in the declaration

For non-payment of personal income tax, a fine is provided, which will amount to 5% of the unpaid tax amount for each month from the date of delay, including incomplete ones. For the absence of a report, if it does not contain the amount of personal income tax payable, the fine will be minimal - 1000 rubles. If there is tax to be paid, you will have to pay a fine of up to 30% of the accrued tax.

03/20/2019, Sashka Bukashka

On February 18, 2018, the order of the Federal Tax Service of Russia dated October 25, 2017 N ММВ-7-11/822@ came into force, which introduced changes to the tax return form for personal income tax (form 3-NDFL). These changes are also valid in 2019 for declaring income received in 2018. Let's look at how to fill out the form taking into account the new requirements.

Personal income tax is a personal income tax paid to the state by working citizens, and is a declaration that is submitted to the tax service by people receiving income in Russia. This article describes how to fill out the 3-NDFL declaration and why it is needed.

Who needs to submit a tax return 3-NDFL

The declaration is submitted upon receipt of income on which personal income tax must be paid, as well as to return part of the tax previously paid to the state. 3-NDFL is submitted:

- Individual entrepreneurs (IP), lawyers, notaries and other specialists who earn their living through private practice. What these people have in common is that they independently calculate taxes and pay them to the budget.

- Tax residents who received income in other states. Tax residents include those citizens who actually live in Russia for at least 183 days a year.

- Citizens who received income from the sale of property: cars, apartments, land, etc.

- Persons who received income under a civil contract or from renting out an apartment.

- Lucky people who win the lottery, slot machines or betting must also pay tax on their winnings.

- If necessary, obtain a tax deduction: for, for, and so on.

Do not confuse this document with . They have similar names and usually come in the same set of documents, but they are still different.

Where to submit the 3-NDFL declaration

The declaration is submitted to the tax service at the place of permanent or temporary registration (registration). It is handed over in person or sent by mail. You can also submit your tax return online. To fill out 3-NDFL online, obtain a login and password to enter the taxpayer’s personal account at any tax office. To receive your login and password, come in person and don’t forget your passport.

Deadlines for filing 3-NDFL in 2019

In 2019, the personal income tax return in Form 3-NDFL is submitted by April 30. If the taxpayer completed and submitted the report before the amendments to the form came into force, he does not need to submit the information again using the new form. If you need to claim a deduction, you can submit your return at any time during the year.

Sample of filling out 3-NDFL in 2019

You will be assisted in filling out the 3-NDFL declaration by the “Declaration” program, which can be downloaded on the website of the Federal Tax Service. If you fill out 3-NDFL by hand, write text and numeric fields (TIN, fractional fields, amounts, etc.) from left to right, starting from the leftmost cell or edge, in capital printed characters. If after filling out the field there are empty cells, dashes are placed in them. For a missing item, dashes are placed in all cells opposite it.

When filling out the declaration, no mistakes or corrections should be made; only black or blue ink is used. If 3-NDFL is filled out on a computer, then the numerical values are aligned to the right. You should print in Courier New font with a size set from 16 to 18. If you do not have one page of a section or sheet of 3-NDFL to reflect all the information, use the required number of additional pages of the same section or sheet.

Amounts are written down indicating kopecks, except for the personal income tax amount, which is rounded to the full ruble - if the amount is less than 50 kopecks, then they are discarded, starting from 50 kopecks and above - rounded to the full ruble. Income or expenses in foreign currency are converted into rubles at the exchange rate of the Central Bank of the Russian Federation on the date of actual receipt of income or expenses. After filling out the required pages of the declaration, do not forget to number the pages in the “Page” field, starting from 001 to the required one in order. All data entered in the declaration must be confirmed by documents, copies of which must be attached to the declaration. To list documents attached to 3-NDFL, you can create a special register.

Instructions for filling out 3-NDFL. Title page

A cap

In the “TIN” paragraph on the title and other completed sheets, the identification number of the taxpayer - an individual or company - is indicated. In the item “Adjustment number”, enter 000 if the declaration is submitted for the first time this year. If you need to submit a corrected document, then 001 is written in the section. “Tax period (code)” is the period of time for which a person reports. If you are reporting for a year, enter the code 34, the first quarter - 21, the first half of the year - 31, nine months - 33. “Reporting tax period” - in this paragraph, indicate only the previous year, the income for which you want to declare. In the “Submitted to the tax authority (code)” field, enter the 4-digit number of the tax authority with which the submitter is registered for tax purposes. The first two digits are the region number, and the last two are the inspection code.

Taxpayer information

In the “Country Code” section, the code of the applicant’s country of citizenship is noted. The code is indicated according to the All-Russian Classifier of Countries of the World. The code of Russia is 643. A stateless person marks 999. “Taxpayer category code” (Appendix No. 1 to the procedure for filling out 3-NDFL):

- IP - 720;

- notary and other persons engaged in private practice - 730;

- lawyer - 740;

- individuals - 760;

- farmer - 770.

The fields “Last name”, “First name”, “Patronymic”, “Date of birth”, “Place of birth” are filled in exactly according to the passport or other identity document.

Information about the identity document

The item “Document type code” (Appendix No. 2 to the procedure for filling out 3-NDFL) is filled in with one of the selected options:

- Passport of a citizen of the Russian Federation - 21;

- Birth certificate - 03;

- Military ID - 07;

- Temporary certificate issued instead of a military ID - 08;

- Passport of a foreign citizen - 10;

- Certificate of consideration of an application to recognize a person as a refugee on the territory of the Russian Federation on its merits - 11;

- Residence permit in the Russian Federation - 12;

- Refugee certificate - 13;

- Temporary identity card of a citizen of the Russian Federation - 14;

- Temporary residence permit in the Russian Federation - 15;

- Certificate of temporary asylum in the Russian Federation - 18;

- Birth certificate issued by an authorized body of a foreign state - 23;

- Identity card of a Russian military personnel/Military ID of a reserve officer - 24;

- Other documents - 91.

The items “ ”, “Date of issue”, “Issued by” are filled out strictly according to the identity document. In “Taxpayer Status,” number 1 means a tax resident of the Russian Federation, 2 means a non-resident of Russia (who lived less than 183 days in the Russian Federation in the year of income declaration).

Taxpayer phone number

In the new form 3-NDFL, fields for indicating the taxpayer’s address have been removed. Now you do not need to indicate this information on the form. Simply fill out the “Contact phone number” field. The telephone number is indicated either mobile or landline, if necessary, with the area code.

Signature and date

On the title page, indicate the total number of completed pages and the number of attachments - supporting documents or their copies. In the lower left part of the first page, the taxpayer (number 1) or his representative (number 2) signs the document and indicates the date of signing. The representative must attach a copy of the document confirming his authority to the declaration.

3 main mistakes in 3-NDFL that we usually make

Expert commentary specifically for Sashka Bukashka’s website:

Evdokia Avdeeva

StroyEnergoResurs, chief accountant

The most common errors can be divided into three groups:

- Technical errors. For example, a taxpayer forgets to sign on required sheets or skips sheets. The tax office will also refuse to provide deductions without supporting documents. The costs of purchasing property, treatment, training, insurance must be confirmed by contracts and payment documents.

- Incorrect or incomplete filling of data. “Top” of such shortcomings:

- on the title page in the line “adjustment number” when submitting the declaration for the first time, put 1, but it should be 0;

- incorrect OKTMO code.

Such shortcomings are not so terrible, and in the worst case they will lead to refusal to accept the declaration. But incompletely filling out some data can lead to the tax office “misunderstanding you” and instead of providing a deduction, it will require you to pay tax.

For example, if the taxpayer in the section “Income received in the Russian Federation” does not indicate the amount of income, the amount of tax calculated and the amount of tax withheld, then instead of refunding the tax, the taxpayer will calculate it for himself as an additional payment.

- Ignorance of laws and rules for applying deductions. For example, a citizen paid for training in 2017, but wants to receive a deduction for 2018. However, the tax benefit is provided specifically for the year in which the applicant paid for education, medical care or other services.

Filling out 3-NDFL when declaring income and filing tax deductions

The procedure for filling out 3-NDFL depends on the specific case for which you are filing a declaration. The declaration form contains 19 sheets, of which you need to fill out the ones you personally need.

- Section 1 “Information on the amounts of tax subject to payment (addition) to the budget/refund from the budget”;

- Section 2 “Calculation of the tax base and the amount of tax on income taxed at the rate (001)”;

- Sheet A “Income from sources in the Russian Federation”;

- Sheet B “Income from sources outside the Russian Federation, taxed at the rate (001)”;

- sheet B “Income received from business, advocacy and private practice”;

- sheet D “Calculation of the amount of income not subject to taxation”;

- Sheet D1 “Calculation of property tax deductions for expenses on new construction or acquisition of real estate”;

- Sheet D2 “Calculation of property tax deductions for income from the sale of property (property rights)”;

- sheet E1 “Calculation of standard and social tax deductions”;

- sheet E2 “Calculation of social tax deductions established by subparagraphs 4 and 5 of paragraph 1 of Article 219 of the Tax Code of the Russian Federation”;

- sheet J “Calculation of professional tax deductions established by paragraphs 2, 3 of Article 221 of the Tax Code of the Russian Federation, as well as tax deductions established by paragraph two of subparagraph 2 of paragraph 2 of Article 220 of the Tax Code of the Russian Federation”;

- sheet 3 “Calculation of taxable income from transactions with securities and transactions with derivative financial instruments”;

- Sheet I “Calculation of taxable income from participation in investment partnerships.”

In addition to paying personal income tax, the declaration will be useful to receive a tax deduction. By law, every citizen can return part of the tax previously paid to the state to cover the costs of education, treatment, purchase of real estate or payment of a mortgage loan. You can submit documents to receive a deduction any day after the end of the year in which the money was spent. The deduction can be received within three years.

Based on Article 216 of the Tax Code of the Russian Federation, every citizen is obliged to report on his income received for the year. In this way, the amount for paying taxes is calculated - the obligation of every citizen on the basis of Article 57 of the Constitution of the Russian Federation. According to Article 229 of the Tax Code of the Russian Federation, information on profits received must be submitted before April 30 of the current year - data for the past year. To report to the tax service, a personal income declaration is filled out. How to do this will be discussed with an example.

Income tax for Russian citizens is calculated annually after submitting a declaration in Form 3 - this document is called a declaration in Form 3-NDFL. The document indicates the income received for a certain period of time.

Declaration 3-NDFL must be submitted by citizens who have a certain income

Who is required to submit

Articles 227, 227.1 and 228 of the Tax Code of the Russian Federation clearly define the list of persons who must report their cash receipts without fail. The list of such taxpayers includes:

- individual entrepreneurs;

- notaries;

- lawyers;

- persons with private activities that generate profit.

In some cases, information about funds received must be submitted by foreigners and non-residents of the Russian Federation.

What income is included?

Having understood what a declaration is, you should consider information about what you will have to pay tax on. In other words, what is meant by the profit received for the year. The income of citizens of the Russian Federation includes:

- remuneration from persons and organizations, with the exception of tax authorities and tax agents;

- funds received from real estate transactions and property rights, if the objects were owned for less than 3 years;

- winnings in cash equivalent in lotteries and other promotions, which are subject to an inflated rate of tax payments;

- remuneration received as an inheritance - this means copyrights, works of art and other similar means;

- profit from activities currently carried out by the taxpayer;

- various cash proceeds received from the sale of securities and other property;

- other income for which no personal income tax was paid.

The elements presented must be supported by a documentary basis. Otherwise, it will be difficult to prove your involvement in a certain amount of money. If the tax authorities discover such an unplanned concealment, the citizen will be brought to administrative or criminal liability (concealment of income on an especially large scale).

Responsibility for late submission

If the income declaration was not submitted on time, administrative liability arises. According to Articles 119 and 122 of the Tax Code of the Russian Federation, if the declaration is submitted later than April 30, the citizen-taxpayer will be issued a fine. If the declaration is submitted on time, but the tax itself is not paid by the due date (July 15), penalties are charged for each day of delay.

Memo from the tax service website

Documents to fill out

Before considering the question of how to fill out a declaration in form 3-NDFL, you should submit the documents that will be needed for independent work. The following documents will be required to complete:

- passport of a citizen who reports for his cash receipts to the tax service; if an electronic version is sent, then it is necessary to provide a scanned copy of the document;

- TIN – it is issued to Russian citizens and individual entrepreneurs;

- agreement on the completed transaction - it must be submitted if the form includes a record of the profit received from the sold property;

- any documents that confirm the fact of receipt of the property - the information provided must also be provided subject to the signing of any agreement on the purchase of real estate;

- certificate of earnings received in form 2-NDFL.

It may be necessary to prepare additional documentation if the situation requires it.

It is better to collect documents for filing a declaration immediately throughout the year in a separate folder immediately after completing any transaction.

Filling example

To know exactly how to fill out the declaration correctly, you need to familiarize yourself with its sample:

In 2017, the existing declaration underwent minor changes, which must be taken into account. Otherwise, the tax service will not accept the completed declaration, arguing that the document is invalid.

Form 3-NDFL consists of a title page and 2 sections - a total of 11 sheets. They should be filled out as required. Next, we will discuss how to fill out the declaration separately, sheet by sheet.

It is possible to fill out a declaration using a special program

Title page

All fields on the title page are filled in with the exception of those allocated for tax service employees. The following information is entered here:

- tax reporting period;

- correction code – when submitting for the first time they put “0”, if not for the first time, then they indicate an attempt in a specific case – “1”, “2”, etc.;

- code of the tax service unit at the place of registration - can be found on the website;

- personal data of the person being filled out;

- information about the taxpayer - date of birth and information from the passport;

- address of place of residence - strictly according to registration;

- applicant’s status – resident or non-resident (has Russian citizenship, but is absent from the country for more than 183 days);

- a valid telephone number for communication;

- declaration sheets that were completed and attached - their number is indicated upon completion of completion;

- if this is required, then information about the taxpayer’s representative is provided;

- signature of the person filling out the document.

The remaining fields are left to be filled out by tax officials.

1 section

In the first section, information is entered after completion of filling out - here the calculated amount of tax is presented based on the fact of the reporting presented below. The section also contains columns that must be filled out:

- 020 – budget classification code – type of income received, information can be taken from the tax service website;

- 030 – OKTMO – territory classifier, which is also determined using the Federal Tax Service website;

- 040 – amount of calculated tax;

- 050 – the amount of refundable previously overpaid tax, in this case “0” is written.

All information on codes is presented on the Federal Tax Service website according to the territorial affiliation of the one being filled out.

Section 2

Next, you should fill out section 2, which includes the amount of funds received. On this sheet, at some points there is even a hint for calculating amounts. There are lines from 010 to 140, which are divided into 2 groups. The first includes information about the tax base, and the second is intended to record the calculated calculations.

Once completed, each section should be checked and signed, indicating the date the declaration was completed.

Sheet “A”

In sheet “A” it is necessary to indicate the sources from which the cash receipts were received. Sources are grouped based on their location in Russia. When filling out, you should indicate the type of income, TIN, KPP and OKTMO source and other information. It is also important to take into account that it is required to indicate the amounts of income not only those that are taxed, but also others that are not subject to taxation.

This is followed by sheets “B”, “C”, “D” and others, which require mandatory completion of the form if other receipts have been received. For example, sheet “B” is filled out only if funds came from sources located outside the territory of Russia. Sheets “3” and “I” are filled out in the same way.

When a declaration is submitted, it is carefully double-checked, since citizens filling out the document for the first time often make mistakes. Full instructions on filling out form 3-NDFL can be viewed on the Federal Tax Service website.

Sample income statement

In independently filling out the income statement for Russian citizens, it is necessary to highlight the following features and recommendations:

- If you cannot fill out the declaration yourself, it is recommended that you turn to professionals. You can also use ready-made programs downloaded from the Federal Tax Service website.

- If the declaration is filled out by an authorized person, then he must have a power of attorney certified by a notary.

- It is important not to violate the specified deadlines. If this year April 30 falls on a weekend, then the due date is extended until the first working day.

- Even if there is no tax liability, a return must be filed anyway.

- In case of delay, the taxpayer will have to pay a fine of at least 100 rubles.

- Making mistakes in a declaration does not always entail a complete refusal to accept it. In this case, a tax officer contacts the taxpayer and points out the error, saying that it needs to be corrected. To do this, submit a new clarifying declaration, filled out in the same sequence and in compliance with the above rules. For the survey to work, you must enable JavaScript in your browser settings.

Income tax return – tax rate, taxpayers and filing deadlines, as well as other important components. Recommendations from a lawyer for drawing up a 3-NDFL declaration and a corresponding sample for filling it out, which can be downloaded for free on our website.

Income tax is the main type of direct tax for citizens of the Russian Federation, calculated as a percentage of the total income of individuals minus documented expenses. As a rule, the income tax of an individual is withheld by a tax agent (for example, an employer), but in some cases the taxpayer is obliged to independently calculate and pay the tax, in these cases a tax return 3-NDFL is filled out.

Income tax rate and objects of taxation

In Russia, for many years there has been a fixed tax rate for the main types of income of an individual - 13%. In this case, basic income means income from hired work, from renting out housing, from work under a contract, etc. In addition, some types of income are subject to different rates: 35, 30 and 9%.

Tax on the income of an individual is calculated if there is a tax base and an object of taxation, which are:

- wage;

- dividends;

- winnings and prizes;

- rental income from real estate;

- income from material benefits and in kind;

- payments under insurance and pension agreements;

- interest on deposits in banks, if the amount exceeds the Central Bank refinancing rate;

- income from the sale of a car, securities and real estate;

- income from the sale of LLC shares and other property.

Important! Income that is not subject to taxation at the income tax rate is listed in Article 217 of the Tax Code of the Russian Federation.

It is worth noting that the taxpayer has the right to take advantage of tax deductions when paying income tax:

Standard- applied monthly in cases established by law.

Social- for training, medicines, pensions.

Property- when selling residential and commercial real estate and other property, when buying housing and land, with interest on targeted housing loans.

Deadlines for filing returns and paying income taxes

According to the general rule in force in the Russian Federation, the 3-NDFL tax return is submitted to the territorial inspectorate at the place of residence no later than April 30 of the current year following the reporting period. Exceptions are defined in paragraph 3 of Art. 229 of the Tax Code of the Russian Federation - if income payments are terminated before the end of the tax period, an individual must submit a report on actual income received to the tax office within five days from the date of termination of payments. The amount of tax calculated on the basis of the information in the taxpayer’s declaration must be paid by him no later than July 15 of the year following the reporting period. If the tax has been additionally assessed, its payment is made no later than 15 days from the date of filing the declaration.

Download tax return form 3-NDFL

The income tax return consists of:

- title page

- several sections that are filled out on separate sheets in order to calculate the tax base and the amount of tax on income taxed at different rates;

Important! The title page and sections 1 and 2 of the declaration must be completed by all taxpayers submitting a report to the inspectorate. The remaining sections are completed only if necessary.

- sheets:

A- all income and sources of their payment within the Russian Federation received during the reporting period are indicated (income from business activities, lawyering and private practice is excluded); B- income and sources of payment outside the Russian Federation are indicated; IN- income from business and advocacy activities, private practice is indicated; G- used to calculate and reflect amounts of income that are not subject to tax; D1- used for calculating property tax deductions for expenses on new construction or acquisition of real estate; D 2- used for calculating property tax deductions for income from the sale of property and property rights; E1- used to calculate standard and social tax deductions; E2- is used to calculate social tax deductions established by subparagraphs 4 and 5 of paragraph 1 of Article 219 of the Tax Code of the Russian Federation, as well as investment tax deductions established by Article 219.1 of the Tax Code of the Russian Federation; AND- is used to calculate professional tax deductions established by paragraphs 2, 3 of Article 221 of the Tax Code of the Russian Federation, as well as tax deductions established by paragraph two of subparagraph 2 of paragraph 2 of Article 220 of the Tax Code of the Russian Federation; Z- used to calculate taxable income from transactions with securities and transactions with derivative financial instruments (DF); AND- used to calculate taxable income from participation in investment partnerships.

Rules for filling out an income tax return

- the document may be completed using software or completed by hand in printed capital characters using blue or black ink;

- at the top of each page of the declaration the number and TIN of the taxpayer, his surname and initials must be indicated;

- at the bottom of each page of the document, with the exception of the title page, the date and signature of the taxpayer must be affixed;

- any amounts indicated in the declaration must have the value of whole rubles when rounding rules are used;

- corrections are not allowed in the declaration, as well as double-sided printing of the document;

- there is no need to print optional declaration pages if they have a zero value;

- The declaration must not be stapled or stapled using any means that may damage the paper.

Important! If an error was made in the return, correcting it is a necessary action for the taxpayer. An updated version of the declaration must also be submitted to the tax authorities as soon as possible.

Methods for filing a return with the tax authorities

Tax return 3-NDFL can be submitted to the inspectorate in the following ways:

- in paper form- 2 copies of the declaration are drawn up, one of which remains with the inspection, the second is given to the person who submitted the declaration with a note of acceptance of the document;

- by mail- the document is sent by registered mail with an inventory attached, the date of sending the letter will be considered the date of filing the declaration;

- electronic- carried out via the Internet using various operators that ensure the exchange of information between taxpayers and the Federal Tax Service.

Most of the income of individuals comes from wages and salaries. On such income, as on many other types of income, tax is withheld and paid by tax agents, usually employers.

However, in some cases, individuals need to independently calculate the amount of tax by submitting a personal income tax return to the tax authority, which calculates the amount of tax payable to the budget. There are many reasons why an individual may be required to submit a declaration to the tax authority - from the sale of property to winning the lottery.

At the same time, the law not only establishes this obligation, but also provides the taxpayer with the opportunity to submit a tax return when an individual has the right to receive tax deductions and a refund of overpaid tax in connection with the emergence of this right.

On the pages of the brochure we will help you find out in which case an individual has an obligation to file an income tax return, how to fill it out correctly, when the personal income tax must be paid, and much more.

INDIVIDUALS INCOME TAX PAYERS

- from sources in the Russian Federation and/or from sources outside the Russian Federation by individuals who are tax residents of the Russian Federation;

- from sources in the Russian Federation by individuals who are not tax residents of the Russian Federation.

Personal income tax (NDFL) is paid on all types of income received in the tax period (calendar year), both in cash and in kind:

When determining the tax status (residency) of an individual, his citizenship does not matter. Thus, a citizen of the Russian Federation can become a tax non-resident, and a foreigner can become a resident. Moreover, during the year, the tax status of an individual may change depending on the time of his stay on the territory of the Russian Federation.

NOTE

Tax residents are individuals who are actually in the Russian Federation for at least 183 calendar days over the next 12 consecutive months. At the same time, the time an individual stays in the Russian Federation is not interrupted by periods of his travel outside the Russian Federation for short-term (less than six months) treatment or training (Clause 2 of Article 207 of the Tax Code). If an individual independently declares the income he received at the end of the tax period, then his tax status is calculated as of December 31. In this case, the days an individual is in Russia before the start of the reporting tax period or after its end are not taken into account (letter of the Federal Tax Service of Russia dated August 30, 2012 No. OA-3-13/3157@).

Regardless of the actual time spent in the Russian Federation, the following are recognized as tax residents:

1. Russian military personnel serving abroad;

2. employees of state authorities and local governments sent to work outside the Russian Federation.

Documents confirming the actual presence of an individual on the territory of the Russian Federation may be:

1. an employment contract or a civil contract, a certificate from the place of work, advance reports with documents confirming expenses, waybills, etc.;

2. an identity document with marks from the border control authorities about crossing the border;

3. if, when crossing the border, entry and exit border control marks are not placed (for example, on the border with Belarus, Kazakhstan, Ukraine), then such documents can be air and railway tickets, hotel receipts;

4. other documents drawn up in the manner prescribed by law, on the basis of which an individual can be considered as a tax resident of the Russian Federation.

How to determine tax status for a citizen of a foreign country

J. Smith arrived in the Russian Federation on January 14, 2013 to perform contract work ordered from him by Romashka LLC.

According to the Tax Code, in order to be recognized as a tax resident of the Russian Federation, J. Smith must remain on the territory of the Russian Federation for at least 183 calendar days over the next 12 consecutive months. J. Smith will become a tax resident of the Russian Federation from July 15, 2013, when the total amount of calendar days in the country will be 183: 18 days in January, 28 -

in February, 31 in March, 30 in April, 31 in May, 30 in June and 15 in July. At the same time, J. Smith will not lose his status as a tax resident of the Russian Federation until the end of 2013.

In accordance with Art. 226 of the Tax Code, the obligation to calculate, withhold and pay the amount of tax in respect of income paid to an individual is assigned to the tax agent, usually the employer. However, in some cases, individuals need to independently calculate the amount of tax by submitting a tax return on personal income tax to the tax authority, in which the amount of tax payable to the budget is calculated. Such individuals include:

1. individual entrepreneurs;

2. notaries, lawyers, arbitration managers and other persons engaged in private practice;

3. individuals who received income:

- from the sale of property (for example, an apartment, a car, etc.) that was owned at the time of sale for less than three years, and property rights;

- in the form of various kinds of winnings (in lotteries, casinos, slot machines, sweepstakes and bookmakers, from participation in promotions, competitions, etc.);

- under civil contracts (for example, income from renting out property);

- in the form of remuneration paid to them as heirs (legal successors) of the authors of works of science, literature, art, as well as authors of inventions, utility models and industrial

- samples;

- as a gift in cash or in kind (real estate, vehicles, shares, shares, shares, etc.) from a person who is not a family member or close relative;

- upon receipt of which the tax agent did not withhold tax, etc.

NOTE

The list of income from sources in the Russian Federation and outside the Russian Federation, from which personal income tax (NDFL) is paid, is given in Art. 208 Tax Code.

TAX RATES

The Tax Code provides for five tax rates on personal income:

1. tax rate of 9%;

2. tax rate of 13%;

3. tax rate of 15%;

4. tax rate of 30%;

5. tax rate of 35%.

LAW AND ORDER

The procedure for applying certain types of tax rates in relation to the income of individuals and categories of taxpayers is established by Art. 224 Tax Code.

The basic personal income tax rate is 13% and applies to most income of individuals who are tax residents of the Russian Federation.

First of all, such income includes wages, the tax on which is calculated, withheld and transferred to the budget by the tax agent, usually the employer.

LAW AND ORDER

Tax agents for personal income tax are Russian organizations, separate divisions of foreign organizations in the Russian Federation, as well as individual entrepreneurs, notaries engaged in private practice, lawyers who have established law offices, from which or as a result of relations with which the taxpayer received income subject to personal income tax (clause 1, Article 226 of the Tax Code)

Income taxed at a rate of 13% also includes remuneration under civil contracts, income from the sale of property, as well as some other types of income.

Taxation at a rate of 9% applies upon receipt of:

1. dividends from individuals who are tax residents of the Russian Federation from equity participation in the activities of organizations;

2. interest on mortgage-backed bonds issued before January 1, 2007;

3. income of the founders of trust management of mortgage coverage based on the acquisition of mortgage participation certificates issued by the mortgage coverage manager before January 1, 2007

What personal income tax rate should I apply to income received in the form of dividends from a foreign company?

Petrov A.K. permanently residing in Ryazan and being a tax resident of the Russian Federation, in 2013 he received income in the form of dividends from a company registered in the Republic of Seychelles to his current account in a Russian bank in US dollars.

According to paragraphs. 1 clause 3 art. 208 of the Tax Code, dividends received from a foreign organization are classified as income received from sources outside the Russian Federation.

With regard to income from equity participation in the activities of organizations received in the form of dividends by individuals who are tax residents of the Russian Federation, a tax rate of 9% is established. Thus, Petrov A.K. must calculate the amount of tax in respect of dividends from a foreign company at a rate of 9%.

The tax rate is set at 35% in relation to:

1. the value of any winnings and prizes received in competitions, games and other events for the purpose of advertising goods, works and services, in amounts exceeding 4,000 rubles;

2. interest income on bank deposits to the extent that the amount of interest accrued in accordance with the terms of the agreement exceeds the amount of interest calculated:

- for ruble deposits - based on the refinancing rate of the Central Bank of the Russian Federation, effective during the period for which the specified interest was accrued, increased by 5%;

- for deposits in foreign currency - based on 9% per annum.

Utkina V.A. took part in a competition held by Romashka LLC and won an LCD TV worth 34,000 rubles.

Since when taxing winnings and prizes in competitions and games held for the purpose of advertising goods, works or services, tax is paid only on amounts exceeding 4,000 rubles, the tax base will be 30,000 rubles. (34,000 rubles - 4,000 rubles), and the amount of personal income tax on winnings is 10,500 rubles. (RUB 30,000 x 35%). If the prize draw was held for the purpose of advertising a manufacturer or seller of goods, the personal income tax on the winnings will be 4,420 rubles. (RUB 34,000 x 13%).

3. income in the form of material benefits received from savings on interest on borrowed (credit) funds in terms of excess:

- for ruble loans (credits) - the amount of interest calculated based on 2/3 of the current refinancing rate established by the Central Bank of the Russian Federation on the date the taxpayer actually received income, over the amount of interest calculated based on the terms of the agreement;

- for foreign currency loans (credits) - the amount of interest calculated on the basis of 9% per annum, over the amount of interest calculated on the basis of the terms of the agreement.

LAW AND ORDER

Material benefits received from savings on interest for the use of borrowed (credit) funds provided for the construction or acquisition on the territory of the Russian Federation of residential real estate (share/stakes in it), land plots for it, are exempt from taxation, provided that the taxpayer has the right to receiving a property tax deduction established by paragraph. 2 p. 1 art. 220 of the Tax Code, and confirmed by the tax authority in the manner prescribed by Art. 3. 220 Tax Code. (Letter from the Russian Ministry of Finance

dated 17.09.2010 No. 03?04?05/6?559)

4. income in the form of fees for the use by the credit consumer cooperative of funds contributed by shareholders, as well as interest for the use by the agricultural credit consumer cooperative of funds raised from shareholders in the form of loans, to the extent that the amount of the specified fee is exceeded, interest accrued in accordance with the terms of the agreement , over the amount of payment, interest, calculated based on the refinancing rate of the Central Bank of the Russian Federation, valid during the period for which the specified interest was accrued, increased by 5%.

The tax rate is set at 30% in relation to all income of individuals who are not tax residents of the Russian Federation, with the exception of income received:

1. in the form of dividends from equity participation in the activities of Russian organizations, in respect of which the tax rate is set at 15%;

2. from carrying out labor activities, in respect of which the tax rate is set at 13%;

3. from carrying out labor activities as a highly qualified specialist in accordance with Federal Law No. 115-FZ dated July 25, 2002 “On the legal status of foreign citizens in the Russian Federation”, in respect of which the tax rate is set at 13%;

LAW AND ORDER

A highly qualified specialist is recognized as a foreign citizen who has work experience, skills or achievements in a specific field of activity, claiming to receive a salary, in particular, in the amount of at least two million rubles for one year (Clause 1, Article 13.2 of Federal Law No. 115- Federal Law).

4. from the implementation of labor activities by participants in the State Program for Assistance to the Voluntary Resettlement of Compatriots Living Abroad to the Russian Federation, as well as members of their families who jointly moved to permanent residence in the Russian Federation, in respect of which the tax rate is set at 13%;

5. from the performance of labor duties by crew members of ships flying the State Flag of the Russian Federation, in respect of which the tax rate is set at 13%.

INCOME EXEMPT FROM TAXATION

The Tax Code establishes a fairly wide list of income that is not subject to taxation (exempt from taxation).

LAW AND ORDER

A complete list of income exempt from taxation is contained in Art. 217 Tax Code.

In particular, the following types of income of individuals are not taxed: state benefits, including unemployment benefits, maternity benefits, as well as other payments and compensation, with the exception of benefits for temporary disability and caring for a sick child;

- state pensions, labor pensions and social supplements to pensions;

- alimony;

- amounts of one-time payments (including in the form of financial assistance);

- scholarships;

- income received from the sale of livestock and crop products grown on private farms;

- income of members of a peasant (farm) enterprise from the production and sale of agricultural products (during the first five years from the moment of registration of the enterprise);

- income of individuals who are tax residents of the Russian Federation, received from the sale of residential houses, apartments, rooms, including privatized residential premises, dachas, garden houses, land plots, share(s) in them, as well as other property, which were in their ownership for three years or more (except for the sale of securities);

- income in cash and in kind received from individuals through inheritance, with the exception of remuneration paid to the heirs (legal successors) of the authors of works of science, literature, art, as well as discoveries, inventions and industrial designs;

- income in cash and in kind received from individuals as a gift, except for cases of donation of real estate, vehicles, shares, shares, shares;

- any gifts received in cash or in kind from a person who is a family member or close relative (spouse or wife, parents and children, adoptive parents and adopted children, grandparents and grandchildren, full and half (having a common father or mother) brothers and sisters );

- prizes in cash and/or in kind received by athletes for winning places;

- the amount of tuition fees for the taxpayer for basic and additional general education and professional educational programs, vocational training and retraining in educational institutions that have the appropriate license and status of an educational institution;

- income in the form of interest received on deposits in banks located on the territory of the Russian Federation;

- maternal (family) capital funds;

- amounts received by taxpayers from the budgets of the budget system of the Russian Federation to reimburse the costs of paying interest on loans (credits);

- amounts of payments for the purchase and/or construction of residential premises provided at the expense of budgets at various levels;

- contributions for co-financing the formation of pension savings, directed to ensure the implementation of state support for the formation of pension savings;

- employer contributions to the funded part of the labor pension in the amount of contributions paid, but not more than 12,000 rubles per year per each employee in whose favor the contributions were paid;

- one-time and urgent pension payments made in the manner established by the Federal Law “On the Procedure for Financing Payments from Pension Savings”.

TAX DEDUCTIONS

Submitting a tax return is not only the responsibility of the taxpayer, but also his right. Thus, individuals who have the right to receive tax deductions for personal income tax can fill out and submit a tax return. A tax deduction is an amount that reduces the amount of income (the so-called tax base) on which tax is paid. In some cases, a tax deduction means the return of part of previously paid income tax for an individual, for example, in connection with the purchase of an apartment, expenses for treatment, education, etc.

NOTE

It is not the entire amount of expenses incurred within the declared deduction that is subject to refund, but the corresponding amount of previously paid tax.

A citizen who:

1. is a tax resident of the Russian Federation;

2. At the same time, he receives income from which personal income tax is withheld at a rate of 13%.

Tax deductions cannot be applied to individuals who are exempt from paying personal income tax due to the fact that they, in principle, have no taxable income. Such persons include:

1. unemployed people who have no other source of income other than state unemployment benefits;

2. individual entrepreneurs who apply special tax regimes and do not have other income taxed at a rate of 13%.

In total, the Tax Code provides for six groups of tax deductions:

1. standard tax deductions (Article 218 of the Tax Code of the Russian Federation):

- deduction for the taxpayer;

- deduction for a child;

2. social tax deductions (Article 219 of the Tax Code of the Russian Federation):

- on expenses for charity;

- on training costs;

- on expenses for treatment and purchase of medicines;

- on expenses for non-state pension provision and voluntary pension insurance;

- on expenses for the funded part of the labor pension;

3. property tax deductions (Article 220 of the Tax Code of the Russian Federation):

- when selling property;

- when purchasing property;

4. professional tax deductions (Article 221 of the Tax Code of the Russian Federation);

5. tax deductions when carrying forward losses from transactions with securities and transactions with financial instruments of futures transactions traded on the organized market (Article 220.1 of the Tax Code of the Russian Federation);

6. tax deductions when carrying forward losses from participation in an investment partnership to future periods (Article 220.2 of the Tax Code of the Russian Federation).

As a general rule, tax deductions for personal income tax are provided at the end of the tax period (calendar year) by the tax inspectorate at the place of residence (place of stay) of an individual when he submits a tax return for personal income tax with the necessary set of documents attached to it.

Lists of documents necessary and sufficient to obtain certain types of tax deductions are given on pages 17-19 of the brochure. When submitting copies of documents confirming the right to deduction to the tax authority, it is recommended to have their originals with you for verification by a tax inspector.

ADVICE

All necessary information about the procedure for obtaining tax deductions is posted on the website of the Federal Tax Service of Russia www.nalog.ru in the section “For individuals”

- Personal income tax, tax deductions

- Deductions

PROCEDURE FOR COMPLETING A TAX DECLARATION

A tax return for personal income tax is a document developed and approved in the prescribed form, with the help of which in the Russian Federation individuals report on the income they receive, the sources of their payment, calculate the amount of tax to be paid or refunded, and declare their right to tax deductions.

LAW AND ORDER

The form of the tax return for personal income tax (3-NDFL) for 2012, the procedure for filling it out and the presentation format were approved by Order of the Federal Tax Service of Russia dated November 10, 2011 No. ММВ-7-3/760@.

The following requirements are presented when filling out a tax return:

- the declaration is filled out by hand or printed on a printer using blue or black ink;

- double-sided printing on paper is not allowed;

- corrections are not allowed;

- deformation of barcodes when printing the declaration and loss of information on the sheets when they are stapled are not allowed;

- each indicator corresponds to one field consisting of a certain number of cells;

- all cost indicators are indicated in the declaration in rubles and kopecks, with the exception of amounts of income from sources outside the territory of the Russian Federation, before their conversion into Russian rubles;

- personal income tax amounts are calculated and indicated in full rubles (values less than 50 kopecks are discarded, values of 50 kopecks or more are rounded to the nearest full ruble).

- text and numeric fields of the form are filled in from left to right, starting from the leftmost cell, or from the left edge of the field reserved for recording the value of the indicator;

- when filling out the indicator “Code according to OKATO (OKTMO)”, the free cells to the right of the code value if the OKATO (OKTMO) code has less than eleven characters are filled with zeros;

- at the top of each page to be filled out is the taxpayer identification number (TIN), as well as his last name and initials in capital letters;

- at the bottom of each page to be filled out, with the exception of the title page, in the field “I confirm the accuracy and completeness of the information indicated on this page,” the signature of the taxpayer or his representative and the date of signing are affixed.

When filling out a declaration, all indicator values are taken from certificates of income and withheld amounts of taxes issued by tax agents, settlement, payment and other documents available to the taxpayer, as well as from calculations made on the basis of these documents.

LAW AND ORDER

Taxpayers have the right not to indicate in the tax return income that is not subject to taxation (exempt from taxation) in accordance with Art. 217 of the Tax Code, as well as income upon receipt of which the tax is fully withheld by tax agents, if this does not prevent the taxpayer from receiving tax deductions provided for in Art. 218 - 221 Tax Code.

If it is discovered in the submitted tax return that information is not reflected or is incompletely reflected, as well as errors leading to an underestimation of the amount of tax payable, the taxpayer must make appropriate changes and submit an updated tax return to the tax authority.

LAW AND ORDER

The taxpayer is released from liability when submitting an updated tax return to the tax authority after the deadline for filing a tax return and the deadline for paying the tax have expired in the cases provided for in Art. 81 Tax Code.

The Declaration form contains the following sheets:

- Title page;

- Sections 1, 2, 3, 4, 5, 6;

- Sheets A, B, C, D1, G2, G3, D, E, G1, G2, G3, G, I.

When filling out the title page of the declaration, indicate:

Taxpayer Identification Number (TIN).

ADVICE

You can find out your TIN on the website of the Federal Tax Service of Russia www.nalog.ru on the “Find out TIN” service page.

Correction number (when filing an initial tax return, the value equal to “0” is indicated, when updating a declaration, the value is indicated according to the serial number of the updating declaration for the corresponding reporting period). The reporting tax period is the calendar year for which the declaration is submitted. Tax authority code - code of the tax office at the taxpayer’s place of residence (place of stay). Taxpayer category code:

- “720” - an individual registered as an individual entrepreneur;

- “730” - a notary engaged in private practice, and other persons engaged in private practice in accordance with the procedure established by current legislation;

- “740” - a lawyer who established a law office;

- “760” - another individual declaring income in accordance with Art. 228 of the Tax Code, as well as for the purpose of obtaining tax deductions in accordance with Art. 218-221 of the Tax Code or for another purpose;

- “770” is an individual registered as an individual entrepreneur and is the head of a peasant (farm) enterprise.

The taxpayer can determine the code of the tax inspectorate and OKATO (OKTMO) at the address of his place of residence (place of stay) using the Internet service “Address and payment details of your inspection”, located on the website of the Federal Tax Service of Russia www.nalog.ru in the “Electronic Services” section .

General information about the taxpayer by filling in the following fields:

- last name, first name and patronymic;

- contact phone number indicating telephone code;

- date and place of birth, citizenship;

- information about the identity document;

- taxpayer status (tax resident/non-resident of the Russian Federation);

- address of residence (place of stay).

Sections 1, 2, 3, 4, 5, 6 are filled out on separate sheets and serve to calculate the tax base and tax amounts on income taxed at various rates, as well as tax amounts subject to payment/addition to the budget or refund from the budget:

In Section 1 on income taxed at a rate of 13%.

In Section 2 on income taxed at a rate of 30%.

In Section 3 on income taxed at a rate of 35%.

In Section 4 on income taxed at a rate of 9%.

In Section 5 on income taxed at a rate of 15%.

Section 6 is completed after completing Sections 1, 2, 3, 4 and 5 of the declaration form.

NOTE

The title page and section 6 of the declaration form are required to be completed by all taxpayers submitting the declaration. Sections 1 – 5 are completed as necessary.

Sheets A, B, C, G1, G2, G3, D, E, G1, G2, G3, Z, I are used to calculate the tax base and tax amounts when filling out sections 1, 2, 3, 4 and 5 of the declaration form and are filled out of necessity:

Sheet A is filled out for taxable income received from sources in the Russian Federation, with the exception of income from business activities, advocacy and private practice. Sheet B is filled out for taxable income received from sources outside the Russian Federation, with the exception of income from business activities, advocacy and private practice. Sheet B is filled out for all income received from business activities, advocacy and private practice.

Sheet D1 is used to calculate and reflect the amounts of income that are not subject to taxation in accordance with a. 7 clause 8 and clauses 28, 33 and 43 art. 217 of the Tax Code (with the exception of income in the form of the value of winnings and prizes received in competitions, games and other events for the purpose of advertising goods (works and services). Sheet D2 is used to calculate and reflect the amounts of income that are not subject to taxation in accordance with paragraph 28 Article 217 of the Tax Code in the form of the value of winnings and prizes received in competitions, games and other events for the purpose of advertising goods (works and services). Sheet G3 is used to calculate the amount of withholding tax on income exempt from taxation in accordance with Subclause 1, Clause 1, Article 212 of the Tax Code.

Sheet D is used to calculate professional tax deductions for royalties established by clause 3 of Art. 221 of the Tax Code, under civil contracts established by paragraph 2 of Art. 221 of the Tax Code, as well as tax deductions for income from the sale of a share in the authorized capital of an organization, upon assignment of rights of claim under an agreement for participation in equity

construction, installed by a. 2 pp. 1 clause 1 art. 220 Tax Code.

Sheet E is used to calculate property taxes

deductions for income from the sale of property, from the seizure

property for state or municipal needs,

established paragraphs. 1 and 11 paragraph 1 art. 220 Tax Code.

Sheet G1 is used to calculate standard tax

deductions established by Art. 218 Tax Code.

Sheet G2 is used to calculate social tax

deductions established by Art. 219 Tax Code.

Sheet G3 is used to calculate social tax

deductions established by paragraphs. 4 paragraphs 1 art. 219 Tax Code.

Sheet 3 is used to calculate the tax base

on transactions with securities and financial

derivatives instruments.

Sheet I is used to calculate property taxes

deductions for the acquisition of property established

pp. 2 p. 1 art. 220 Tax Code.

NOTE

All the necessary information on the procedure for filling out the tax return form for personal income tax in form 3-NDFL is posted on the website of the Federal Tax Service of Russia www.nalog.ru in the “Documents” section.

There are several options for filling out the declaration:

- in paper form using a declaration form filled out by hand;

- in electronic form using an electronic form;

- using the Declaration 20__ program.

When filling out the declaration by hand, the form fields are filled in with capital printed characters, and, in the absence of any indicator, a dash is entered in the cells of the corresponding field. When preparing a declaration in electronic form, the values of numerical indicators are aligned to the right (last) space; when printing on a printer, it is allowed that there is no framing of cells or dashes for unfilled cells. Signs are printed in Courier New font with a height of 16-18 points.

LAW AND ORDER

In accordance with paragraph 3 of Art. 80 of the Tax Code, the tax authority provides tax return forms (including in electronic form) free of charge.

The most convenient and simplest way to fill out a declaration is to use the “Declaration 20__” program, designed to automatically fill out a personal income tax return for the corresponding year. To use the “Declaration 20__” program, the taxpayer only needs to enter the initial data, on the basis of which the program will not only automatically generate declaration sheets for all taxable income received from sources in the Russian Federation and received from sources outside the Russian Federation, but will also calculate tax amounts for payment or return from the budget.

TAX RETURN DEADLINES